Can you consider light as a product, ready to pick up from the shelf and take home? You can't touch or hold it, but being able to use it whenever needed has been vital to the progress of humanity. Light sources have progressed from candles and oil lamps to incandescent and fluorescent bulbs, becoming ever more controllable and economical. The amount of light that humanity has “consumed” has consistently increased throughout these transitions, increasing our productivity and wealth in the process, note Jeff Tsao and his colleagues.

“Light is a good thing – it makes us more productive,” says Tsao, chief scientist at the Energy Frontier Research Center for Solid-State-Lighting Science at Sandia National Labs in the US. “If luminous efficacy increases and cost of light decreases, people can consume more light on the same budget and become even more productive than they were before.” Now, with a transition to solid-state lighting dawning, Tsao and his colleagues have tried to answer questions of critical interest to manufacturers involved in the field. How much LED light will people consume for illumination, and how much equipment will be needed to make the LEDs to provide it?

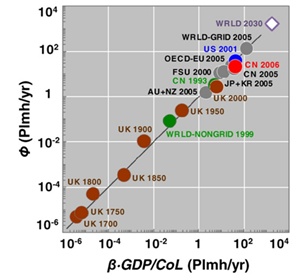

The Sandia team has found that countries have consistently spent 0.72 percent of their GDP on artificial lighting. If this continues to hold true in the future, it looks like good news for companies seeking to sell LEDs and the means to produce them. “There are two baselines that one can construct. One is that the consumption of light is basically saturated,” Tsao says. In this scenario, the amount of light humans currently use is essentially all we will ever need to use. Not only does this impose an upper limit on the number of LEDs needed, but the more efficient LEDs become, the fewer are needed to satisfy demand.

Putting rival technologies in the shade

Cheaper lumens

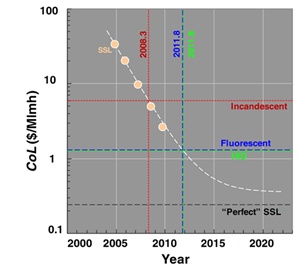

Of course, humans could choose to consume more light by spending the same amount on cheaper lumens. “It assumes the future will be different to the past,” Tsao pointed out. “We thought we'd see what would happen if the future behaved like the past.” The Sandia team looked at what this would mean for the world in 2030, compared to the world in 2005, based on a number of assumptions on what will change in this time. As well as assuming that spending on artificial light will remain a constant percentage of GDP, they assume annual GDP will grow from $61 trillion to $137 trillion, that the cost of electricity will remain roughly constant, and that, thanks to the transition to solid-state emitters, the luminous efficacy of artificial lighting technology would increase from 48 lm/W to 268 lm/W.

Given this scenario, the Sandia team predicts that world consumption of light will increase from 131 Plmh/yr to 1,688 Plmh/yr. If LED lamps used to produce this light are operated at 200 A/cm2 current density and 1/4 duty cycle, they would require LED chips covering a total area of 1.31 km2, they say. Tsao emphasizes, though, that he and his colleagues are agnostic about whether or not the future will be like the past. “The purpose of our work was simply to understand what the future would be like, if it were like the past,” he says.

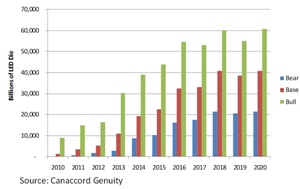

LED demand forecast

Tool time

If the expected change from existing technology to solid-state lighting takes place over 10 years, and the LEDs could be produced at 75% yield, 0.17 km2 worth of die would need to be produced per year, Tsao and colleagues calculate. The semiconductor material for LEDs is typically deposited using a technique known as metalorganic chemical vapor deposition (MOCVD). On the basis of the Sandia team's model, “the estimated semiconductor chip area turnover required during the transition to SSL would require the equivalent of roughly 1800 MOCVD tools,” they write in the Journal of Physics D: Applied Physics.

That paper cites figures from market analysts IMS Research suggesting that 1,413 MOVCD tools were in use at the end of 2009, indicating that it's likely this will need to at least double to meet the additional demand for LEDs used in solid state lighting. IMS Research itself suggests that over 1600 new reactors will be needed to meet the demand for solid state lighting between 2010-2020, assuming that 1 mm x 1 mm chips become the de facto standard. But despite predicting a very similar outcome to Sandia, IMS makes some very different assumptions to get there. These reflect the current maturity of LED technology, compared to the future progress predicted by Tsao's team.

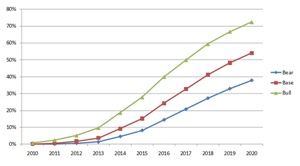

Lighting market penetration

According to Ross Young, senior vice president, displays, LEDs and lighting at IMS, LED yields of 75 percent are not typical today, and his company's models assume 50 percent. “We've heard as low as 10 percent, and as high as 90 percent,” he says. Yields are being negatively impacted, Young notes, by LED manufacturers such as Cree, who are increasing the size of their LED chips to improve their luminous efficacy at higher driving currents. To help accommodate that size increase, the company is also moving to a larger wafer size, of 6-inch diameter. LED epiwafers usually have a number of “device-killing” defects. Using fewer, larger die rather than more, smaller die means that a higher proportion of them are affected by these defects. “The larger the area of the die, the more likely it is that there will be a yield problem, compared with smaller die,” Young explains.

As the analyst also points out, not every installed MOCVD tool is fully utilized – something that is especially true in China currently. “They're subsidising MOCVD equipment to the tune of even 60%,” he says, citing the Chinese government’s generous subsidizing of LED manufacturing in the country.. “But the equipment isn't going to be utilized to the same degree as it is in Taiwan, Korea and Japan. There are limitations on what they're going to be able to sell outside China due to intellectual property issues.”

Tooling up

Socket to 'em

IMS Research references a recent Canaccord Genuity report that models calculated LED demand from solid-state lighting based on the existing number of light sockets, converted into lumens, and then the number of die needed, assuming that efficacy figures start near 100 lm/W and increase to 200 lm/W. “On that basis, there'll be a need for over 1600 new 12 x 4-inch MOCVD tools required to meet lighting demand,” Young said. “However, the total MOCVD market will likely be significantly larger if one accounts for replacement tools as new, more productive tools are introduced as well as non-lighting demand and the under-utilization of subsidized tools in China.”

There are differences between the various models. Canaccord Genuity's forecast assumes that solid-state fixtures will claim a maximum of 70% of the overall lighting market, while Sandia's assumes that they will completely dominate. One key obstacle to achieving penetration, Young notes, is the price of the whole LED lighting fixture – significantly more than the emitter alone. Manufacturing tools have a key role to play in this area, since improved epitaxy and more efficient chips require less cooling. MOCVD systems that significantly improve throughput, uniformity and yield will drive fixture prices down further.

“We expect to see cluster tools introduced in the near future that significantly boost throughput while minimizing footprint, and reduce wafer costs”, Young said. The emergence of these systems is, in part, tied to the impending and long-anticipated entry of mainstream semiconductor manufacturing giant Applied Materials into the LED arena. However, neither of the existing leading MOCVD tool manufacturers, Veeco Instruments and Aixtron, are resting on their laurels of what Young calls their current duopoly. “They're trying to out-duel each other to get costs down and grow the overall market,” the IMS researcher says. “They're continuing to reduce the tools' cost of ownership, with Aixtron introducing a higher throughput system in 2010, and Veeco set to introduce a more productive system in 2011. Veeco’s roadmap calls for them to introduce new MOCVD systems every 12-18 months.”

The potential for LEDs to penetrate further into the lighting market could mean that even more MOCVD tools than IMS' current estimates are ultimately needed. But, while Young thinks it will be important to consider how LEDs affect the way that we use light, he does not necessarily think that the amount of light consumed will increase greatly. “For residential lighting, people might leave their lights on more, but I don't think you're going to see more sockets,” he says. “I think people are happy to replace existing lamps, perhaps leave the lamp on more, but I don't think that we're going to see more sockets.”