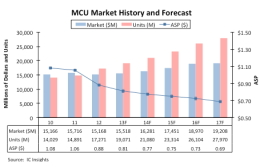

In 2012, MCU unit shipments surged 16%, but total revenues declined 3% and ASPs plunged 17%, says IC Insights.

While uncertainty about the global economy played a factor in lowering MCU revenues, the market was significantly undermined by price erosion in 2012 as competition intensified in 32-bit microcontrollers.

The 17% drop in ASPs was the worst one-year decline for MCUs since the 1980s. Meanwhile, MCU shipments climbed to a new record high of 17.3 billion in 2012, but the strong increase was not enough to keep dollar-volume sales from falling 3% to $15.2 billion.

The pervasiveness of MCUs means that their market growth has been relatively stable since the 1980s compared to many other IC product categories.

It typically takes a global economic recession to upset the diverse MCU marketplace, and that's exactly what occurred in 2009, when the microcontroller business suffered its worst-ever annual sales decline of 22% to $11.1 billion.

Coming out of the 2009 downturn, MCU sales roared back with a record-high 36% increase in the 2010, but thereafter, the microcontroller market has lost momentum as the world's economy wobbled forward.

IC Insights believes the microcontroller market will return to "normalcy" in the next few years. Microcontroller sales are forecast to rise 2% in 2013 and reach $15.5 billion with unit shipments growing 10% to nearly 19.1 billion (a new record high).

Price erosion in MCUs is expected to ease in 2013 with ASPs dropping 8%. MCU sales and unit shipments are forecast to steadily gain strength each year between 2014 and 2016 before growth rates substantially slow in 2017. Between 2012 and 2017, MCU revenues are projected to increase by a compound annual growth rate (CAGR) of 4.8% while unit shipments are expected to rise by a CAGR of 10.1% over the five-year period.

Globally, some softness continues to persist in computer markets, consumer goods, and industrial segments, but the bright spots for 2013 MCU growth can be found in communication applications, automotive electronics, smartcards, medical equipment, home automation, power management and smart metering, solid-state lighting built with light emitting diodes (LEDs), and renewable-energy generation, such as solar systems and wind turbines.

Historically, the 8-bit segment has dominated MCU sales, but as shown in Figure 2, the 32-bit segment became the leading segment of the MCU market in 2010. The difference between 4-/8- and 32-bit MCU sales was just $235 million in 2010, but the size gap has grown much wider since then. The 32-bit microcontroller segment is forecast to reach nearly $6.9 billion in 2013, 57% larger than the size of the 4 /8-bit MCU market.

In terms of unit shipments, 16-bit microcontrollers became the largest volume MCU category in 2011, overtaking 8-bit devices for the first time that year. Shipments of 16-bit MCUs grew 11% in 2012 after a 23% increase in 2011, partly on the strength of automotive applications.

In 2013, 16-bit MCU shipments are expected to rise 9% to 7.9 billion units. Shipments of 4-/8-bit MCUs are expected to grow 6% to 6.7 billion in 2013. Meanwhile, 32-bit MCU shipments are forecast to climb by 20% in 2013 to 4.5 billion units.

IC Insights believes the makeup of the MCU market will undergo substantial changes in the next five years with 32-bit devices steadily grabbing a greater share of sales and unit volumes.

By 2017, 32-bit MCUs are expected to account for 55% of microcontroller sales, while 16-bit devices will represent 22% of market revenues and 4-/8-bit will be about 23%, based on IC Insights' forecast.

In terms of unit volumes, 32-bit MCUs are expected account for 38% of microcontroller shipments in 2017, while 16-bit devices will represent 34% of the total, and 4-/8-bit designs are forecast to be 28% of units sold that year.

The 32-bit MCU market is expected to grow rapidly due to increasing demand for higher levels of precision in embedded-processing systems and the growth in connectivity using the Internet. In the important automotive market, the need for 32-bit processing in MCUs is being driven by the advent of "intelligent" car systems and increases in sophisticated, real-time sensor functions for government-mandated electronic stability control (ESC) and crash-avoidance systems.

Semi-autonomous driving features in cars--such as self-parking, advanced cruise controls, and collision-avoidance systems--are increasing the role of controllers and sensors in new vehicles.

A growing number of automakers are hoping to expand on driver-assist features appearing in cars today to develop "smart" fully autonomous (driverless) vehicles over the next 10 years. In the next few years, complex 32-bit MCUs are expected to account for over 25% of the processing power in vehicles.

A growing number of MCU suppliers are offering new product families based on 32-bit RISC-processor cores licensed from ARM Ltd., which began pursuing the microcontroller segment about eight years ago.

ARM has quickly established a major position in the MCU market by offering intellectual property (IP) and design technologies that are similar to RISC-core technologies used in most application processors for cellphones and tablet computers.

ARM's rapid penetration into the MCU arena has caused a number of microcontroller market leaders to respond.

In Japan, Renesas has been attempting to unify its three 32-bit microcontroller families into a single processor architecture to compete with the onslaught of ARM-core designs, but in 4Q12, Renesas revealed that it would join others offering MCUs with ARM cores.

Renesas joins Freescale, TI, NXP, ST, and many other companies who, after competing with ARM-based microcontrollers for several years, changed course and introduced their own families of ARM-based controllers.