Tilly’s, Inc. reported third-quarter earnings slid 16.4 percent to $5.1 million, or 18 cents per share as selling, general and administrative costs grew 15.4 percent, or more than twice as fast as net sales, which grew 6.1 percent. Same-store sales decreased 1.2 percent.

“We are pleased with the meaningful progress we are making on our initiatives to increase sales and profitability as our third quarter results exceeded expectations," said Daniel Griesemer, president and chief executive officer. “While we recognize there is more work to be done, we are encouraged that our focus on product differentiation and innovation, and improved digital capabilities, in conjunction with a slightly better teen retail environment, are contributing to a general improvement in customer response. These efforts, as well as strong inventory management, resulted in increased product margins in the quarter. Our product offering continued to resonate well with our customer through November, giving us confidence that we are well positioned for the remaining holiday selling season.”

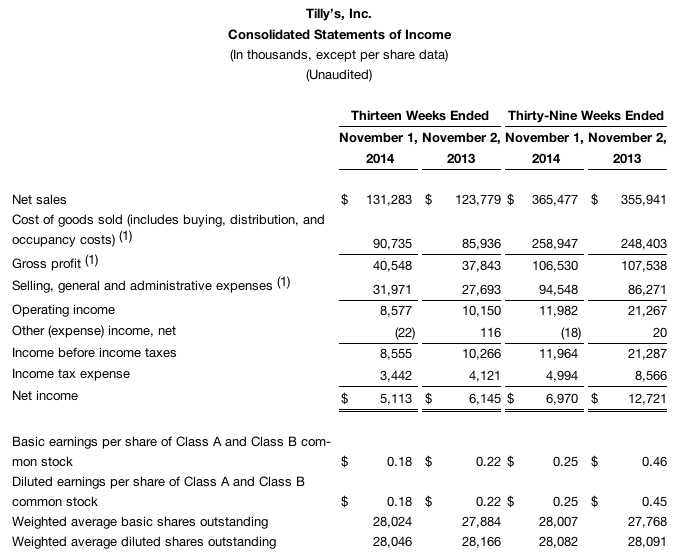

For the third quarter ended Nov. 1, 2014:

Total net sales were $131.3 million compared to $123.8 million in the third quarter of 2013.Comparable store sales, which include e-commerce sales, decreased 1.2 percent compared to the same 13-week period in 2013.Gross profit increased 7.1 percent to $40.5 million compared to $37.8 million in the third quarter of 2013. Gross margin was 30.9 percent compared to 30.6 percent in the third quarter of 2013, primarily due to a 30 basis point increase in product margins.SG&A grew 15.4 percent to 24.3 percent of net sales, up 190 basis points from 22.4 percent in the third quarter of 2013.

Operating income was $8.6 million compared to operating income of $10.2 million in the third quarter of 2013.Net income was $5.1 million, or $0.18 per diluted share, based on a weighted average diluted share count of 28.0 million shares and an effective tax rate of 40.2 percent. This compares to net income in the third quarter of 2013 of $6.1 million, or $0.22 per diluted share, based on a weighted average diluted share count of 28.2 million shares and an effective tax rate of 40.1 percent.For the thirty-nine weeks ended Nov. 1, 2014:

Total net sales were $365.5 million compared to $355.9 million for the first three quarters of the prior year.Comparable store sales, which include e-commerce sales, decreased 5.0 percent compared to the first three quarters of 2013.Gross profit decreased 0.9 percent to $106.5 million compared to $107.5 million in the first three quarters of 2013. Gross margin was 29.1 percent, compared to 30.2 percent in the prior year period. Product margins increased 20 basis points, offset by higher occupancy costs as a percentage of net sales due to the negative comparable store sales.Operating income was $12.0 million compared to $21.3 million in the first three quarters of 2013.Net income was $7.0 million, or $0.25 per diluted share, based on a weighted average diluted share count of 28.1 million shares. This compares to net income in the first three quarters of 2013 of $12.7 million, or $0.45 per diluted share, based on a weighted average diluted share count of 28.1 million shares.Balance Sheet and Liquidity

As of Nov. 1, 2014, the company had $61.3 million of cash and marketable securities and no borrowings or debt outstanding on its revolving credit facility.

Fourth Quarter 2014 Outlook

The company expects fourth quarter comparable store sales to be flat to negative low single digits, and net income per diluted share to be in the range of $0.15 to $0.19. This assumes an anticipated effective tax rate of approximately 40 percent and a weighted average diluted share count of 28.1 million shares. Fourth quarter 2013 net income per diluted share was $0.19, based on a weighted average diluted share count of 28.2 million shares.