Posted by Rick Lingle, Technical Editor -- Packaging Digest, 2/25/2013 3:07:41 PM

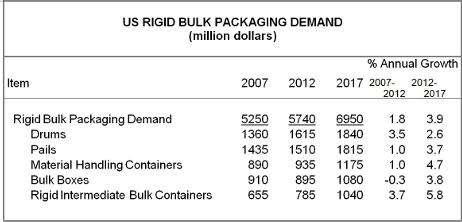

Demand for rigid bulk packaging is forecast to advance 3.9 percent per year to $7.0 billion in 2017, accelerating from the performance of the 2007-2012 period. The improved outlook is based on a recovery in the overall economy, particularly in the motor vehicle and construction markets - which were the hardest-hit segments during the 2007-2009 recession.

This recovery will also spur turnarounds in output of chemical products, fabricated metal products, and plastic materials, which will boost demand for related bulk packaging. Additionally, gains will be driven by expanded use of larger, higher value containers that offer enhanced performance and are more cost effective than smaller containers with shorter term service capability.

Moreover, while the long term trend of outsourcing manufacturing to lower cost regions has lessened the share of the U.S. manufacturing sector in the overall economy, the development of abundant natural gas supplies is expected to fuel increased investment in U.S. chemical production as well as that of related downstream goods, which will have a positive impact on rigid bulk packaging demand. Plastic accounts for the largest share of material use in rigid bulk packaging, with steel and paperboard also significant. These and other trends are presented in Rigid Bulk Packaging, a new study from The Freedonia Group, Inc., a Cleveland-based industry market research firm.

Rigid intermediate bulk containers (RIBCs) and material handling containers are expected to experience the fastest growth through 2017. Opportunities for RIBCs will be supported by a rebound in chemical production as well as advantages of cost effectiveness and reusability. Material handling container growth will be driven by an upswing in production of durable goods such as motor vehicles and fabricated metal products following declines during the 2007-2012 period.

In addition, plastic drums are forecast to log above average gains as a result of advantages over steel drums in terms of cost, weight, and corrosion resistance. However, competition from RIBCs as well as the entrenched position of steel and fibre drums in certain applications will moderate advances. Despite the maturity of steel and fibre drums, drums will remain a widely used rigid bulk packaging type as a result of their relatively low cost, reusability, effectiveness in the safe transport of hazardous materials, and appeal to users not wishing to transition to intermediate bulk containers.