“The most valuable commodity I know of is information.”

(Gordon Gecko in “Wall Street” by Oliver Stone)

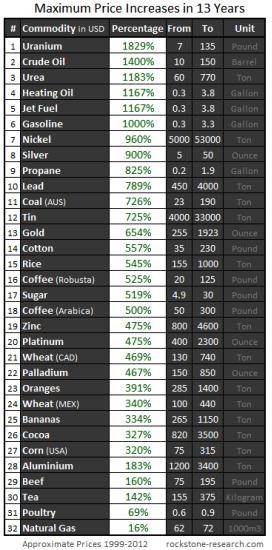

Commodities have experienced a renaissance after the bursting of the internet bubble at the end of the 20thcentury. The new and long-term upward trend began with most commodities in late 1990s and already lasts nearly 15 years. During this time, most commodity prices manifold strongly. The following table presents the maximum price increases of selected commodities since 1999:

Indeed, these were all pretty formidable price increases (except of natural gas) – however, also frightening at the same time. Formidable of course for investors who diagnosed correctly and timely the start of the bull market in commodities now sitting on luscious profits potentially chilling the champagne now. Yet simultaneously frightening, because what if the boom has come to an end? Are those formidable profits on the verge of being vanished into thin air? Wouldn’t it be better to sell and realize profits?

Potential new investors face similar frightening questions: Getting in now? What if the all-time highs are already behind us? What if the bubble was punctured recently and is ready to burst now? What if the globalized world economies are standing on somewhat healthy feet again after the successfully passed finance, euro and Greece crises? Shouldn’t one buy when the blood flows ankle-high and sell when the corks are popping? Is the stuff with the blood already behind us or still in front of us?

Furthermore, a highly used argument against commodities is that they can bring extreme profits solely thanks to an increased volatility that is driven by short-sighted speculators, hedge funds and other kinds of grasshoppers. An increased volatility – per definition a large price range – is also valued negatively as being unpredictable like the tempers of a diva. And when comparing with other “classical investments”, the risk-reward ratio is said to be not as prettily balanced as with bonds, stocks or fixed-income securities.

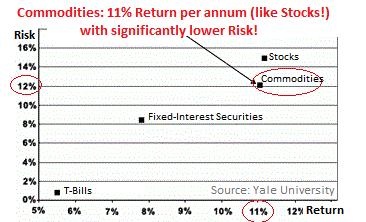

However, the Yale University calculated and empirically prove that in the long run, commodities yield an average profit of 11% per year, which is about the same as for stocks. Yet the risk is significantly lower with commodities than with stocks. This study was completed in 2004, thus at a time when the commodity boom just started and the real strong price increases were to follow.

Against stocks, commodities have the advantage that they can not go bankrupt, there are no quarterly conference calls, no earnings warnings, no criminal management boards, no balance-sheet doctors and no gimmicks. As for commodities, the facts lie straight on the table and it’s all just about supply and demand – and not about hot air. Thus, the question must only be: how have supply and demand developed and where are they heading to?

In the following, we will briefly sketch 4 drivers that make commodities an increasingly scarce resource leading to the conclusion that the commodities boom is not only a typical long-term 10-20 years market cycle, but at least a megatrend.

Demand Driver #1: DEMOGRAPHICS

On average, every second 3 people are born these days. Until 2020, some 500 million people will be born, whereas around 75% will come to earth in Asia. The UN calculated the world population to increase from currently 7 to 9 billion until 2050. These 2 billion new people, or 30% more than today, represent on average 1 million new humans per week coming to earth.

Additionally, another trend is active: urbanization, which is people increasingly leaving rural and undeveloped regions to move into cities. In cities, the per capita consumption of commodities is significantly higher than in the countryside. Calculations forecast that in 2050, some 6.5 billion people will live in cities – today it is only 3.5 billion. These 3 billion new people, or 86% more than today, represent on average 1.5 million people more per week living in cities.

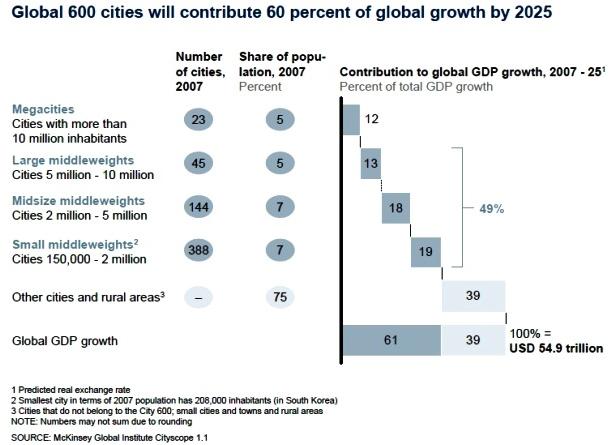

In 2007, out of the 600 strongest GDP-contributing cities in the world, 380 contributed 60% of global economic growth. McKinsey Global Institute (MGI) found out that by 2025, around 600 cities will contribute 61% of global GDP-growth, whereas only 24% of the world population will live in these cities. During the next 13 years, a minimum of 136 new cities will emerge in the current Top-600, whereas all of them will come from developing countries (e.g. 100 cities from China, 13 cities from India and 8 cities from Latin America). The enlargement of all cities in the world until 2050 is expected to equal the combined areas of Germany, France and Spain.

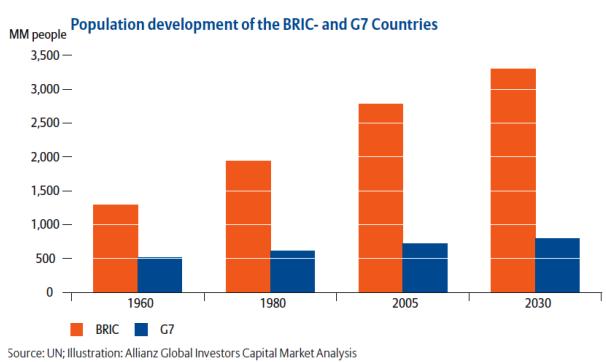

Jim O’Neil (Chief Economist with Goldman Sachs) coined the abbreviation BRIC which stands for the emerging countries Brazil, Russia, India and China, whereas some prefer adding a “S” for South-Africa (“official member” since 12/23/2010). Since years, these countries show extraordinarily strong economic growth between 5-10% per year. Around 2.8 billion people, or 40% of all humans, live in the 4 BRIC countries, yet their contribution to the global GDP was solely 22% in 2008 – however, with a strong tendency to improve significantly over the coming years.

The economic stagnation in most industrialized nations is one of the best-selling arguments for steering the focus of investors on BRICs resulting in an increased number of financial products being emitted (coined) on those markets (not only by Goldman Sachs). Occasionally, the abbreviation BRIICS is referred to representing Brazil, Russia, India, Indonesia, China and South-Africa, or BRICK with Korea (although South-Korea already represents a developed industrial nation, yet still achieving above average growth rates continuously) or Kazakhstan (not only because of high growth rates and an increasing role as an energy supplier, but especially since Kazakhstan is located geographically between the classic BRIC countries opportunely in view of an Eurasian-Pacific prospect). In the case of Russia, some experts are still indecisive as authors like Peter Scholl-Latour rather negatively value the Russian Federation (due to a decreasing population, obsolete industries and infrastructure, and complex social conflicts). Another version is BRICSAM (Brazil, Russia, India, South-Africa, ASEAN and Mexico).

Demand Driver #2: WEALTH

The need for commodities not only increases with a quantitatively growing world population, but also qualitatively, because with higher wealth/incomes the consumption gets more commodity intensive. Those who walk today will buy a bicycle tomorrow – those who cycle today will switch to a car tomorrow. The more people on earth have an income and the more these incomes increase, the more is the demand for commodities. The World Bank forecasts per capita incomes in undeveloped countries to rise twice as strongly as in OECD countries during the next decades. Actually, the real per capita incomes in Asia rose by 90% between 1999-2009.

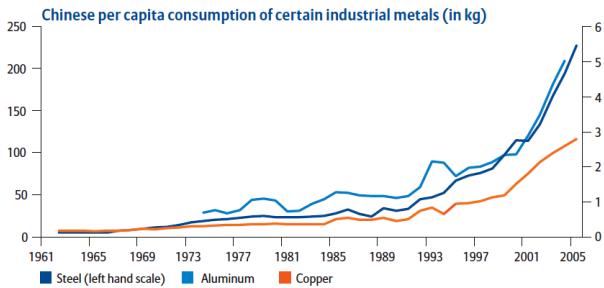

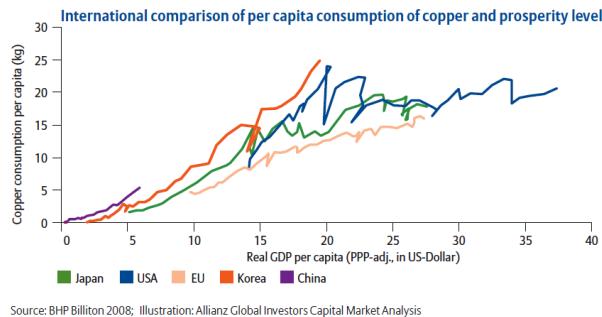

Alone the Chinese hunger for commodities provides for a permanently strong demand, whereas – most interestingly – it already seems “huge” in absolute numbers: The most populated country in the world is already the largest consumer of many commodities, such as copper, aluminium, steel and iron ore. The Chinese per capita consumption of copper, aluminium and steel more than tripled over the last 13 years. Do you know how much copper you consume every year? A German on average 16 kg. However, a Chinese only 3 kg. Or steel: a German currently needs some 465 kg per year, while the Chinese only require 271 kg per head. Such differences are (still) really huge; but how “megahuge” will (absolute) demand seem when the (relative) gap has converged?

China is, after the USA, the 2nd largest importer of oil (around 4 million barrels per day which represents 13% of the total OPEC production), although 4 times as many people live in China than in USA. And although China did not need to important any oil until 1994 (currently 5th largest oil producer), they grew to the 2nd largest oil importer in less than 20 years. A German currently consumes on average around 1,800 liters oil per year, an American more than 4,000 liters, whereas Mexicans not even require 1,000 liters per head. And how much oil does an average Chinese consume? Less than 330 liters.

Energy commodities are somewhat to be differentiated from other commodity groups as the strong oil dependencies of the world may (sooner or later) be substituted with alternative energies. In Brazil, some 25 million cars run on ethanol instead of petroleum – this already represents a Brazilian market share of around 80%. Knowingly, China subsidizes/forces the advance of electro- and alternatively-run cars, because the government understands that their people better not consume even 1,000 liters oil per head per year in the future, because virtually half of all the OPEC production would be necessary to achieve this.

No matter if oil gets increasingly substituted with other energies in the future, the trend typically remains the same: commodities can only be replaced with other commodities (e.g. when price is too high, supply too scarce, or politics against it). Thus, it may not only be profitable to speculate on strong future oil prices, but also on higher sugar prices over the coming decades, or on metals of the rare earth elements (REE) group that are/were used in hybrid cars, such as dysprosium which price rose from 118 in 2008 to 2,300 dollar/kg last year (+1,849%). However, strongly rising prices go in hand with analogous risks as the recent price drop of neodymium, which REE metal is also used in hybrid cars magnets, has shown: from 338 in 2011 to 200 dollar/kg in early 2012 (-41%).

Principally, if prices get too high and/or the supply is too scarce, it makes no sense for an industry to demand that commodity, thus rather looking or trying to innovate for substitution possibilities. For example: “Toyota has developed a technology to substitute rare earths used in its hybrid vehicles.” Recently, China has limited its REE exports as it rather keeps them for itself to develop its markets, which is seen to be totally legitimate – especially if China’s mining output represents >90% of the total world supply. “Hitachi has built an 11-kilowatt motor that uses no rare earth materials… commercial production is expected in 2 years”. However, not every commodity can be substituted by other commodities, as for example silver, which industrial metal has unique characteristics and being classified as not-substitutable in many of its few thousand application fields, thus making its demand rather price inelastic (if price increases manifold, industries will not demand less). Thus, it may not only be profitable to speculate on strong future REE prices, but also on higher prices of those commodities that are replacing REE in hybrid cars.

The Chinese population consensus of 2010 had the result of 1.4 billion people living in the world’s 4th largest country (after Russia, Canada and USA). China still is a country in which the larger portion of its residents lives in poverty. However, some 600 million people managed to get out of extreme poverty between 1981-2005. The success in fighting poverty commenced with the economic reforms in 1978. Between 1981-2001, the number of Chinese living below the breadline (“minimum living wage” or “margin of subsistence”) decreased from 53% to 8%. Surely, the question of definition for “breadline” now emerges: for rural Chinese, it stands at around 100 euro, while urban people are defined with around 135 euro (nota bene: per year). This is less than the broadly propagated margin of 1 dollar per day. According to the UN, around 35% of all Chinese live with less than 2 dollar per day and 10% with less than 1 dollar (in 2007). At least 300 million Chinese in rural areas still do not have access to (clean) drinking water, whereas some 60 million people alone in Southeast-Asian still live with contaminated drinking water. Currently, there are only 200 million Chinese who enjoy a yearly income exceeding 4,000 dollar. However, when comparing with 2003, this represents a 3-fold increase within a single decade.

By no means, China is to be considered as the only country with such a capacious need for commodities. Just think of India, where the government chases its own (very ambitiously) set goal of quadrupling the number of car owners within only 5 years. “India is an emerging power in the 21st century, and is forecasted to become the 3rd largest economy in the world. India is a source of talent and innovation… India supports a vibrant, pluralistic democracy and insists on an open and free press.”

The population consensus of 2011 had the result of 1.2 billion people living in India – which is almost as many as in China, however with one “small” difference: India inheres a much stronger population growth than China. Currently, India’s population grows by 1.5% per year – relatively, this growth rate is just a bit more than the world average, however: in absolute terms, India – with 18 million more people per year – records the largest increase in the world. According to forecasts, India’s population growth is not likely to weaken at all during the next decades and is expected to overtake China as the most populated country in the world by no later than 2025. Most interestingly, the Indian population growth is not explained with an increased birth rate, but with an increased life expectancy which translates into a reduction of the mortality rate. Predominately, this is the result of an increased standard of living respectively wealth.

According to the World Bank, around 44% of all Indian habitants have less than 1 dollar per day to live on. No matter if the nutrition situation has been improved remarkably since the 1970s, more than 25% of the population is still too poor to be able to afford a sufficient feeding. However, the mid- to long-term economic growth perspectives are considered in various cases as positive. Many studies result in the same conclusion, namely that India’s economy will grow stronger than China. Irrespective of the huge catch up that is still required especially in the fields of infrastructure, it is the Indian population pyramid age structure that speaks in favor for a persistent economic growth. The actual high number of young Indians is set to result in a much higher share of people with incomes. The average age of the Indian population stood at 25 years in 2006.

In short: The strongly growing world population – hand in hand with human's intrinsic drive of increasing one's standard of living especially in undeveloped countries – speaks one language, namely that the commodity boom is not at all solely a temporary cyclical phenomenon.

Countries that emerge and develop themselves require commodities. No commodities – no development. No development – no prosperity.

Demand Driver #3: INFRASTRUCTURE

The urban development trend (urbanization) especially in undeveloped countries is set to additionally escalate the demand dynamics for commodities. In times of internet and smart phones, commodities also dominate the everyday life of members of an affluent society as the worldwide development of infrastructure over the last decades has proven (already, the internet in the USA eats up more than 10% of the total US energy demand). New markets and industries, as well as emerging countries, foremost demand buildings, structures and transportation routes, such as streets, rails, waterways and airports, besides all kinds of new facilities that, for example, provide the supply of water and electricity.

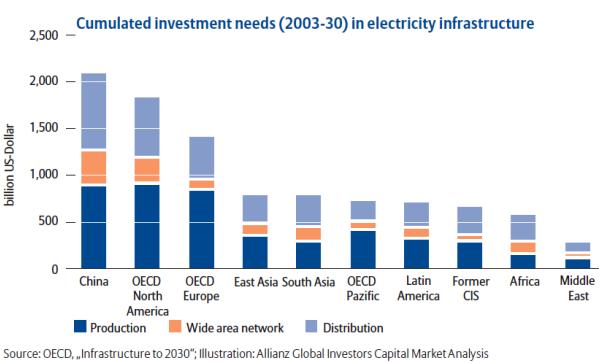

Hence, all these emerging countries, markets and aspiring people are in need of more and more commodities. The increasing number of people on earth is also pressing for an urgently needed water infrastructure as only 80% of all humans are fortunate to use clean water, whereas only 60% have access to sanitary facilities. The OECD estimates a yearly investment requirement for worldwide infrastructure projects in the area of 600 billion dollar for the next 20 years – only to guarantee the provision of water. Additionally, the OECD expects China to spend some 2,000 billion dollar until 2030 for infrastructure only to produce and distribute energy.

However, such cost-intensive infrastructure developments are not only limited to undeveloped countries. As per the OECD, the USA and Canada must invest around 1,800 billion dollar in its electricity facilities, which is almost as much as China. The consequences of a scruffy infrastructure has been shown effectively and exemplary not only with California, but as well with South-Africa, where mines had to be shut down temporarily, because no sufficient supply with electricity was provided. “The Government of India plans to invest over 1 trillion dollar over the next 5 years to meet the country's huge infrastructure demands. Over 50% of these funds will come from the private sector.” Any development of infrastructure is highly commodity intensive.

Price Driver #4: LIMITED SUPPLY

As if the increasing demand from every nook and corner of the world wasn't enough, we must additionally try to realize the crude fact that the supply of commodities can not be increased arbitrarily nor user-defined (in stark contrast to the money supply for example). Firstly, most commodities are not renewable, but limited (“scarce”). Secondly, the most and largest deposits have already been discovered. Surely, there still exist some undiscovered deposits (especially at depth) and it is also known that planet earth perpetually produces new deposits. Hence, the only problem is that our planet simply just needs a couple million years to form most kinds of deposits and that we will have exploited most deposits one day. This is (hopefully) the reason why it is commonly argued that planet earth's resources are limited on a quantity basis, although de facto they sure do “regrow” respectively form in earth's crust continuously. (1

It has become problematic that hardly any new capacities were created over the last years. Since 2002, virtually no large ore discoveries were achieved. The exploration and development of new deposits is getting increasingly difficult and cost-intensive, because – thanks to technological breakthroughs since the 1970s – most deposits have already been discovered near the earth's surface. The BP disaster in front of US coasts showed what kind of risks are already taken and what prices are already taken into (balance sheet) account to try to satisfy demand. Also most oil deposits near earth's surface have been found already plus increasingly running dry, hence we must go deeper (or stop demanding price-inelastically). (2)

Already in 1972, the Club of Rome pointed to the problem that natural resources are limited and that the world's economies are growing disproportionately strong. Despite correct revealing of facts, the markets disavowed them, which may be explained by technological innovations and advances flying high since the 1970s and actually having successfully discovered many new and large deposits while at the same time efficiency in mining significantly increased. It was these technological breakthroughs, coupled with success in exploration, that gave the impression that the supply with commodities is secured for way more than 100 years. The perception of an abundant supply was underpinned with the severe economic crisis in Asia and Russia in the 1990s which negatively impacted other emerging countries as well. It was forecasted that emerging countries would fall out as a demand driver for an undetermined long time.

Consequently, prices for most commodities in the 1990s traded at its lowest levels since more than 100 years (under consideration of inflation). Thanks to this drop in prices, expenditures for the exploration and development of new deposits shrank accordingly. Additionally, it was way more attractive and lucrative to invest in the new and “exciting” markets of the Internet Revolution and the New Era of Information – instead of primitively digging in the dirt for some commodities. At times of the new millennium, not many students had the courage to look at old rocks becoming something as unpopular as a petrographer studying “old-fashioned mining” in face of most companions going to college to avidly study something hip like IT or Marketing & Sales majoring in Communications. The not-so-funny consequence today is that the mining industry dramatically lacks qualified personnel which leads to many projects being developed slower and everyone being penalized with higher commodity prices (besides millions of unemployed communications experts spending their days in modern public placement service centers like Facebook at least giving them a virtual room in the not-so-funny reality to let them do what they studied and thus know best, namely to network and promote brands socially with wit coupled with their own “award-winning innovation” for their underlying industry: for free).

Such thinking and acting is also reflected in the exploration expenditures for new deposits (mining companies even reduced their investments at the end of the 1990s). Of course, exploration investments increased strongly during the current bull market. However, the uncanny to shocking result is that – despite newest state-of-the-art technologies, modern methods and unlimited quantities of money – no large deposits are discovered anymore being the reason why most funds (2008: 73%) are invested in already known deposits and its peripheries. The general perception of an abundant commodity supply seems to have only started to change during the last decade.

Although commodity prices suffered severely with drops of up to 70% during the financial crisis in 2008, most prices recovered to pre-crisis levels as quickly as they dropped. However, most real price levels of the 1970s and 1980s have not yet been reached even closely. When comparing with the past commodity bull cycles, one shall keep always in mind that today's (longer-termed) trend of rising commodity prices has gained vastly in quality, because while most commodities were abundantly available during the last bull markets and price increases were caused typically solely by (short-term) external shocks, such as the Oil Crisis of 1973 and 1979 or the Gulf War in 1990, today it is (more than ever) the dynamic demand – especially from emerging countries – that drive prices up for an indeterminable long time.

On the other side, supply can not keep up with the dynamic global demand. The consequence is inescapable and omnipresent: the supply has become the bottleneck and commodities are becoming an increasingly scarce property respectively a real value. If demand today is bigger than supply, the price will rise tomorrow. Since supply is so scarce, demand can only be slowed down via higher prices, whereas most interestingly, demand keeps on going its way up unimpressed despite commodity prices having increased manifold during the last 13 years. What seems to be in the making is a truly new phenomenon to many commodity markets, namely that demand is becoming price inelastic meaning that demand does not effectively change if prices rise much – as the hunger for development and improvement of standards of living is much stronger. On the other hand, exporting countries like China not only virtually sit on warehouses full of dollar “reserves”.

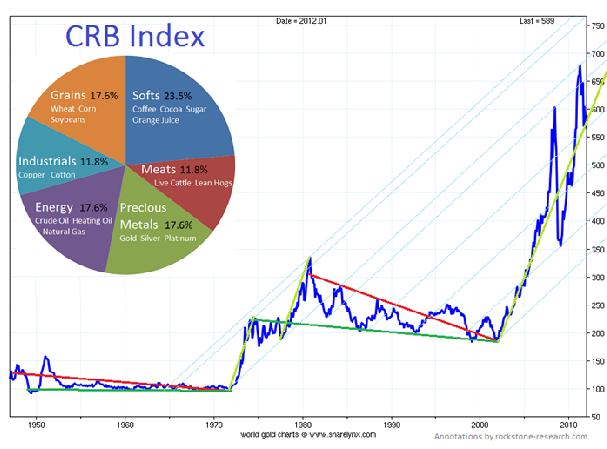

The CRB index was launched in 1957 and is the oldest commodity index on which financial products are emitted. At its birth, the CRB contained 28 commodities having changed to only 17 today (so far, 10 revisions took place). As the following chart since the end of the 1940s suggests, there were 2 strong price increases (so-called “thrusts”) which started after 20 year long sideways-consolidations within (red-green) triangles. While the 1st thrust in early 1970s started at 100 points and found its high at around 350 points (3.5-fold increase) after almost 10 years, the 2nd thrust started in early 2000s at 200 points and found a recent high at 700 points (also 3.5-fold increase) after also around 10 years. Hence, the opinion can be made fast that the commodity boom has now ended.

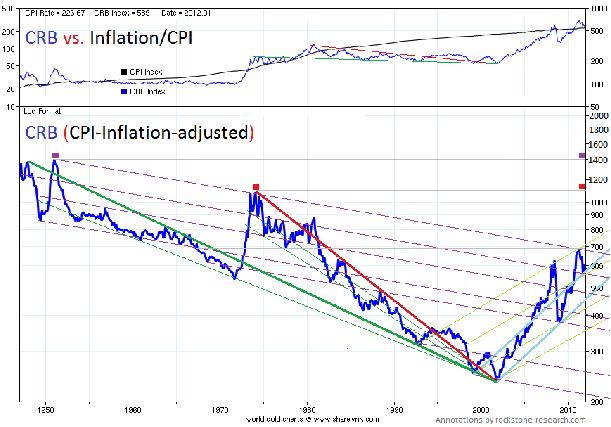

However, the above CRB chart solely shows the nominal development. If one wants to find out, for example, the approximate high of the last bull market with today's purchasing power (value) of the dollar, the below chart should be looked at. It is presented that the real high of the last bull market was already reached in mid-1970s (and not in the end of the decade) – and that the high represents nearly 1,200 points (in today's terms). In order to only reach the real high of the last bull cycle, the CRB would need to trade twice as much today. It also strikes the eye that the CRB reached an even higher high (1,400 points) in the 1950s and that – for real – commodities actually became cheaper during the last 65 years.

Technically, the next major buy-signal for commodities is generated when rising and holding above the uppermost (violet) downward trend-channel currently at approx. 700 points, because a new and longer-termed upward trend is typical thereafter. More importantly to note however is that the increase in prices since the new millennium is the result (“thrust”) of the previous red-green triangle – and that the defined goal of such a thrust is to rise above the high of the triangle (approx. 1,200 points) and transform it into new support in order for a new and longer-termed upward trend to begin thereafter.

Hence, when trying to technically evaluate if commodities are currently “expensive”, not only the nominal price developments must be taken into account, but more importantly the real price developments. One can not say that commodities are “expensive” only because they rose strongly in price. The correct wording would be that commodities became “more expensive” (yet simultaneously they still can be dirt cheap), whereas the current commodity prices have finally just reached the same price level from which the commodities bull of the early 1970s actually started in real terms.

Taking a look at the inflation-adjusted and indexed CRB index since 1921, it becomes also clear what kind of a potential the commodity prices still have (in real comparison with the past) respectively that the upward trend does not stand at the end, but rather at the beginning – and that the really strong price appreciations are yet to come.

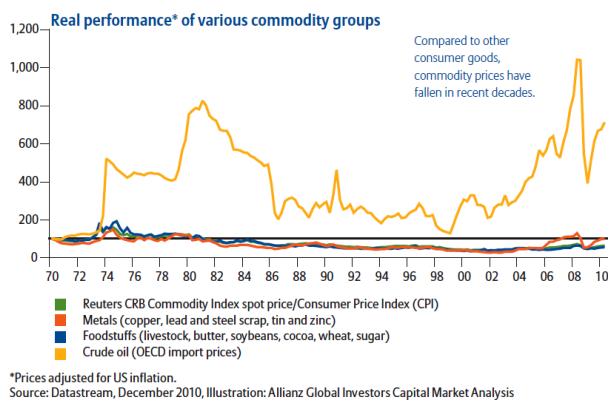

The next graph presents and compares the real and indexed price development of some commodity groups since 1970. It becomes apparent that the oil price not only rose strongly, but that it also behaves quite volatile and seemingly incalculable, whereas all other commodities actually became cheaper during the last 40 years. It goes without saying that there shouldn’t be anyone saying that commodities are within a bubble (if anything oil).

Inflation-adjusted prices are out of touch with reality? The exact opposite must be the case. The same modus operandi is commonly used in everyday finance when calculating so-called real interest rates. If your bank generously pays you a fixed interest of 2% for leaving your money unused as “savings” on your bank account and inflation runs 4% that year, your real interest rate is minus 2%. Thus, your money does not grow by 2% per year, but you really lose 2%.

The next picture shows the gold price (orange; left axis in dollar/ounce) and the real interest rates of 10 year US-Treasury bonds (black; right axis in percent/year). Here, the official inflation rate (CPI) was deducted from the nominal interest rate. As can be seen without fail, the real interest rates of T-bonds are negative at the moment. One may notice additionally that the gold price performed extraordinarily well in times of negative interest rates and very well in times below 2%.

In light of the strongly growing world population especially in emerging countries – coupled with the natural and thus inexorable drive of humans to improve their standards of living – the question when staring at the vanishing commodity supply must not be when the commodity boom will end, but rather if at all the boom can come to an end.

Science-fiction projects like Planetary Resources from James Cameron are helpful in assisting that the general public only slowly realizes the full investment potential of commodities – especially if commodity prices rise stronger than ever now. These unlimited extraterrestrial resource occurrences are thought to hover above the finite terrestrial supply like a Damocles Sword. As commonly known, hope dies last.