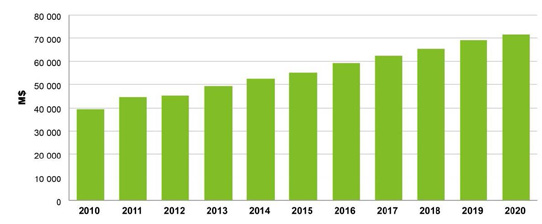

The inverter market grew significantly to $45bn in 2012, and will reach $71bn by 2020, according to Yole Développement in a report on ‘Inverter market trends for 2013-2020 and major technology changes’. “More than 28 million units were shipped in 2012 and we estimate that will grow to 80 million units in 2020,” says Brice Le Gouic, activity leader, Power Electronics, at Yole.

The report provides a focus on the six most attractive motion and conversion applications applications – photovoltaics (PV), wind turbines, electric and hybrid-electric vehicles (EV/HEV), rail traction, motor drives and uninterruptible power supplies (UPS) – and a new analysis on the trends in power stacks from the previous report.

Yole says that energy-related topics (vehicle electrification, renewable energies, electricity transportation) have become more important in 2012. As a direct result, the power electronics market has risen. This growth is driven by: high-volume and cost-pressure applications such as EV/HEV; and high-added-value markets such as renewable energy and rail traction.

Picture: Inverter market (in US$m), for applications including PV, wind turbine, rail traction, EV/HEV, motor drives and UPS.

The main components of inverters – passive and semiconductor modules (found in power stacks) – represent enticing industries, says Yole. In 2012, the market was $1.9bn for power modules and more than $4bn for passive components, including capacitors, resistors, connectors, bus-bars and - newly added in this updated report - magnetic components (inductors and transformers).

Yole notes that, as expected, wide-bandgap semiconductor devices have also started to penetrate those high-end market segments: in particular, silicon carbide (SiC) is present in PV inverters – a total market size of $43m, driven primarily by diodes in micro-inverters but also by junction field-effect transistors (JFETs) – and gallium nitride (GaN) should be introduced to the market in 2013.

Semiconductor technology developments continue to sharpen inverter performance

Yole’s 2012 investigation confirmed that improvements in semiconductors have enabled more efficient conversion, lighter systems and more reliable end-products. For example, silicon-based insulated-gate bipolar transistors (IGBTs) have improved (higher current density, thinner and faster), as have SiC- and GaN-based devices.

GaN could be delayed in its market introduction, notes Yole, but SiC is already here and several companies have demonstrated SiC power module capabilities during last year. Consequently, in the new report Yole has updated its technology roadmaps for materials and devices.

Adoption of power stacks driving modular approach across applications

The report also highlights the trend in power stacks that Yole surveyed closely in 2012. The power stack is the innovative sub-system of an inverter that involves the custom design and manufacturing of an inverter’s sub-unit, which includes only the core components: power semiconductor module, cooling system, capacitors, resistors, current sensors, busbars and connectors.

Yole remarks that inverter and device makers are becoming power stack manufacturers for several reasons, including: vertical integration; access to several applications (since power stacks are less application-dependent than inverters); internal cost reductions; access to high-end markets; and maintaining R&D in-house.

Large firms such as Ingeteam, Semikron or ABB are now involved, but power stacks also interest smaller players such as AgileSwitch (former IGBT driver manufacturer), who are part of this market of about $500m.

Major changes happening across the supply chain

Power electronics often requires having knowledge and experience-based expertise in several different sectors, including mechanics, electronics, semiconductors, electrics, fluidics and hydraulics, and connectors. Development can hence be complicated and final products expensive. As a consequence, Yole has observed and analyzed two main trends coming out of the power electronics industry, as follows.

Japanese and Chinese players (especially system makers) tend toward internal vertical integration, and master the manufacturing processes of each sub-system and component. In the case of Japanese companies, this tendency is driven mostly by cost reduction and the absorption of intermediary margins, whereas Chinese companies want to access the technology and show some proof of quality, says Yole.

On the other hand, EU and US players are diversified, and the acquisition of new or complementary competencies (e.g. Mersen, Rogers or Power Integration) or high-end R&D and prototyping services (APEI, Primes, IMEC, GE Global Research) is becoming more common, concludes the market research firm.