Yole Développement announced today its new report “UV LEDs: Technology & Application Trends” which presents UV LED new applications and associated market metrics for the period 2012-2020, and a deep analysis of UV LED technology and UV LED lighting industry.

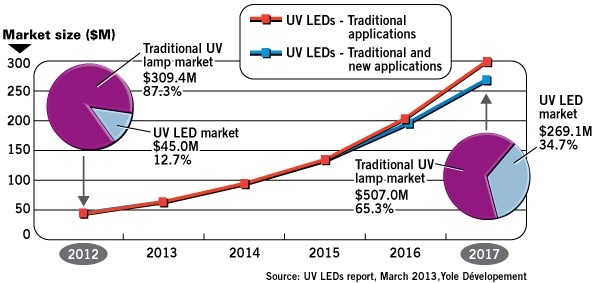

Thanks to UV curing, UV LEDs should become a $270M business by 2017, and could hit $300M if new applications boom

Thanks to its compactness, low cost of ownership and environmentally-friendly composition, UV LED continues to replace incumbent technologies like mercury. Hence, the UV LED business is expected to grow from $45M in 2012 to nearly $270M by 2017, at a CAGR of 43% -- whereas the traditional UV lamps market will grow at a CAGR of 10% during the same time period.

In 2012, UVA/UVB applications represented 89% of the overall UV LED market. Amongst these applications, UV curing is the most dynamic and most important market, due to significant advantages offered over traditional technologies (lower cost of ownership, system miniaturization, etc.). This trend is reinforced by the whole supply chain, which is pushing for the technology’s adoption: from UV LED module and system manufacturers to ink formulators and (of course) the associations created to promote the technology. And with Heraeus Noblelight’s recent acquisition of Fusion UV (Jan. 2013), all major UV curing system manufacturers are now involved in the UV LED technology transition.

Concerning UVC applications, they are still in their infancy and their sales are mainly for R&D purposes and analytic instruments like spectrophotometers. But given some newly published results (increase of EQE over 10%, etc.) and the recent commercialization of the world’s first UVC LED-based disinfection system (2012), the market should kick into gear within the next two years.

In addition to traditional applications (UV lamps replacement), and due to their unique properties (compactness, higher lifetime, robustness, etc.), UV LEDs are also creating new applications that aren’t accessible to traditional UV lamps, i.e. apps that are miniaturized and portable.

“In 2012, several new UV LED based products were launched, including cell phone disinfection systems, nail gel curing systems and miniaturized counterfeit money detectors - and this is likely to continue!” explains announced Pars Mukish, Technology & Market Analyst, LED, at Yole Développement. “We estimate that if new UV LED applications continue emerging, the associated business could represent nearly $30M by 2017, which would increase the overall UV LED market size to nearly $300M,” he adds.

This market and technology analysis is a comprehensive review of every UV application (including a deep analysis of UV curing and UV disinfection purification), highlighting: UV working principle, market structure, UV LED market drivers and the challenges/characteristics associated, time-to-market, penetration rate & Total Accessible Market (TAM) for UV LEDs, and much more. Additionally, Yole Développement details the market metrics for traditional UV lamps and UV LEDs over the period 2012 - 2017, with splits by application for each technology (volume & market size, etc.).

The report also presents an analysis of emerging UV LED applications, detailing: short-term applications that have already begun emerging, UV LED Concept Knowledge theory, and more.

Once UVC LED performance is sufficient, the supply chain battle will intensify

The booming UVA/UVB market (mostly UV curing) has attracted several new players from different backgrounds over the past few years: traditional UV lamp suppliers, traditional UV system suppliers, pure UV LED system suppliers, and others. Each player employs a different strategy for capturing the maximum value created by this disruptive technology: horizontal integration (from UV lamp to UV LED), vertical integration (from UV LED device to UV LED system and vice-versa) or both (from UV lamp to UV LED system). We should point out that traditional UV lamp manufacturers are under the most pressure since they have to compensate for the waning lamp replacement market by diversifying their activities in higher supply chain levels.

In the end, every UV LED device/system manufacturer faces the same technical issues when it comes to integrating UV LEDs into a system (thermal management, optics, etc.), but experience is gained with each passing year. Once UVC LEDs achieve sufficient performance, there’s no way a manufacturer will allow the opportunity to pass them by. When that moment comes, the whole supply chain will become a mess due to an increasingly competitive environment, and consolidation will be necessary. Yole Développement analysis covers the UV LED industry, detailing: main players & associated strategies/business models, 2012 industrial value & supply chains, key players’ revenue and market share, and much more.

Bulk AlN vs. AlN on sapphire template: no current winner

AlN on sapphire templates are definitely the substrate of choice for UVA applications, as they provide the right mix between cost and performance. However, for UVC applications (and some UVB applications) the competition with bulk AlN substrate is strong, since such material could allow for improvement at the device level in terms of lifetime, efficiency (IQE and EQE) and power output.

Right now, the debate is still on. And even if bulk AlN’s superior performance has been demonstrated by companies such as Crystal-IS and HexaTech, the associated cost (2.5x to 4x more compared to AlN on Sapphire template) still remains an obstacle to developing UVC LEDs at a reasonable price.

Indeed, such a situation has already occurred with GaN substrate for visible LEDs. Bulk GaN was the ideal technical candidate, but cost was too high and sapphire was widely adopted instead. Will UV LEDs meet the same fate?

In addition to substrate issues for UVC LED development, epitaxy represents another challenge for increasing device performance. Such barriers will have to be surpassed before we see commercialized UV LED-based disinfection/purification systems.