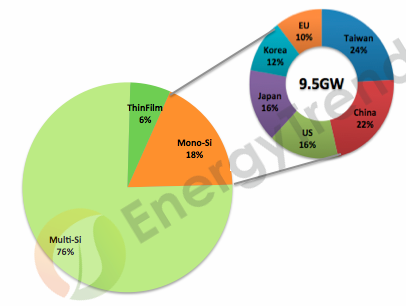

The sluggish growth of the mono-Si market this year is notable given the fact that many cell manufacturers had switched from multi-Si to mono-Si production in the second half of 2014. Statistical research conducted by EnergyTrend for the 2015 PV market finds that even though the global demand has reached 53GW, the total mono-Si cell shipments worldwide may be lower than 10GW. Cost is the deciding factor as to whether or not the mono-Si market can achieve higher growth in the future.

According to EnergyTrend’s annual mono-Si cell shipment forecast for 2015, Taiwan as the leading producing country may surpass 2GW. Major Chinese cell manufacturers including JA Solar, Suntech, and DMEGC will push their country’s mono-Si cell shipments to 2GW. Other regional markets – the U.S., Europe, South Korea and Japan – will ship around 1GW~1.5GW respectively. Major mono-Si cell manufacturers in those regions include SunPower from the U.S., SolarWorld from Europe, LGE from South Korea, and Japan’s Sharp and Panasonic. Taken together, this year’s global mono-Si cell shipments are estimated to be under 10GW. The picture is starkly different in the multi-Si market, where cell manufacturers have been seeing a surge in orders and high capacity utilization rates for multi-Si cell production. Currently, just about 10% of the top-tier global cell manufacturers’ combined capacity is devoted to mono-Si products.

Figure 1: Total mono-Si cell demand and shipments in 2015

Source: EnergyTrend

Mono-Si products are overcoming their weaknesses

For companies developing mono-Si products with higher efficiency, the good news is that the distributed generation (DG) markets in the U.S., the U.K., and Japan have kept growing. However, prices of mono-Si modules remain much higher compared with prices of multi-Si modules. Moreover, P-type mono-Si products come with inherent disadvantages of having higher cell-to-module (CTM) loss and higher light-induced degradation (LID). Using passivated emitter rear cell (PERC) process during the mono-Si cell production significantly raises the products’ conversion efficiency rates, but the technology also increases LID from the average 2% to 3~6%. N-type mono-Si cells by contrast do not suffer from LID. However, they have lower production yield rates and less price flexibility. Producing N-type mono-Si cells also requires additional equipment. Hence, N-type mono-Si products have yet to become the market mainstream due to high costs, and they may need another two or three years become popular.

Since the second half of 2015, cell manufacturers have gradually overcome the mentioned disadvantages of P-type mono-Si cells (pricing, CTM loss, and LID). Demand for P-type mono-Si cell is therefore likely to pick up as better solutions to LID become available and the mono- versus multi-Si price difference in the p-type cell market starts to narrow. In fact, prices of mono- and multi-Si cells in the Chinese market have been almost identical in recent times.

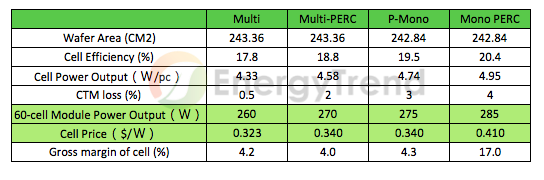

Costs of P-type mono-Si cells have also been lowered substantially this year following the Chinese New Year holidays. During this period, the weak demand for mono-Si products caused excess inventory for mono-Si wafer manufacturers and forced them to sharply reduce their prices. By the second half of 2015, multi-Si wafers stayed at US$0.82~0.83/pc on average, whereas the average price of mono-Si wafers had dropped from US$ 1.05/pc to US$ 0.92/pc. Therefore, the price gap between mono- and multi-Si in the wafer market has contracted from US$0.18~0.20/pc to US$0.10/pc. Moreover, the average manufacturing cost difference between mono- and multi-Si cells is now at US$ 0.015/W. These factors along with higher conversion efficiency rates have resulted in mono-Si cells reaching a dominant position in generation costs (see table 1).

Table 1: Cost and profit comparison between mono- and multi-Si cells

Source: EnergyTrend

Wafer and cell industries have each developed ways to solve LID. Wafer manufacturers focus on reducing the boron-oxygen complex that is the main contributor to LID. Aside from reducing the amount of oxygen in the wafer, manufacturers can also change the dopant. For instance, they can adopt gallium doping or boron and gallium co-doping. Meanwhile, cell manufacturers have begun to add an annealing procedure in their production. Among the equipment used for the annealing process, Germany-based Centrotherm’s regenerator units are the most popular. Recently, Taiwanese cell companies have implemented the annealing procedure and found that LID in mono-Si PERC products have been considerably reduced to within 2%. Wafer and cell companies nonetheless still have a way to before their technological solutions achieve maturity.

Policies and PERC will help accelerate mono-Si demand

Although mono-Si products have become as competitive as multi-Si products in terms of C/P ratio, they require additional stimuli to win larger market share. Currently, national renewable policies in major PV markets are moving towards subsidy reduction. The U.K. and Japan for instance are going to revise their feed-in tariffs (FiT), while the U.S. will make a big cut to its investment tax credit (ITC) for PV systems. These subsidy reductions increase major market’s reliance on DG systems. China, the current leader in PV demand, continues to come up with new subsidies for the DG market. Furthermore, the Chinese government also initiates a new plan called the “Top Runner” program that is expected to give a big boost to mono-Si demand.

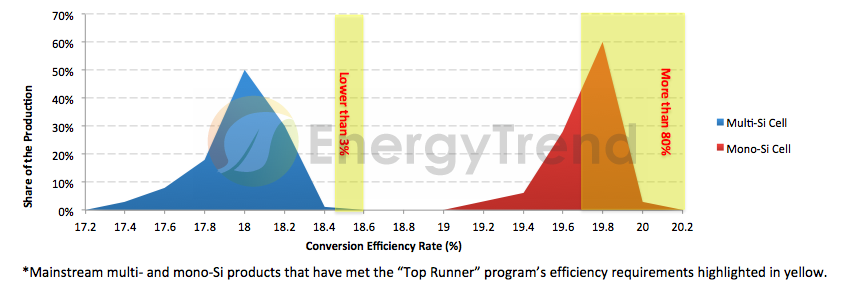

The “Top Runner” program aims to raise the efficiency of Chinese PV products by setting higher requirements for modules used in demonstration projects and encouraging manufacturers to adopt these standards. In this case, the minimum conversion efficiency rates set for multi- and mono-Si modules are respectively at 16.5% and 17.5%. Based on these rates, multi-Si modules would have to generate 270W to meet the standard, whereas the required wattage for mono-Si modules would be 275W. Currently, it is relatively easy for mainstream mono-Si modules to achieve the program’s target since their wattages are typically around 270~275W. On the other hand, the wattage of multi-Si modules is generally around 260W. To comply with the standard, multi-Si products will have to rely on technologies such as PERC or reactive ion etching (RIE).

Recently, the Chinese government has announced the implementation of demonstration project in Datong City as part of the “Top Runner” program. The project, which is located in the coal-mining subsidence areas of the city, will have a total installed capacity of 3GW. The first phase of this project will begin construction soon and is scheduled for completion by the middle of next year. It is expected that the “Top Runner” program and related projects such as this will raise both the demand and profile of mono-Si products in 2016.

Figure 2: Distribution of production for multi- and mono-Si cells based on efficiency rates.

Source: EnergyTrend

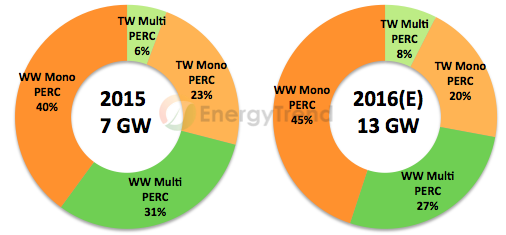

Furthermore, EnergyTrend estimates that the global PERC capacity in total will exceed 13GW in 2016. Since mono-Si cells achieve greater efficiency improvement with the PERC technology, the global PERC capacity for mono-Si products is projected to grow and reach 8GW. Many cell manufacturers that have just installed PERC equipment may have to undergo an adjustment period before going into mass production. However, major companies such as JA Solar and SolarWorld will be able to contribute greatly to the global PERC capacity along with technologically matured Taiwanese cell companies.

Figure 3: PERC capacity distribution for multi- and mono-Si products worldwide and in Taiwan, 2015~2016

Source: EnergyTrend

Mono-Si market outlook for 2016

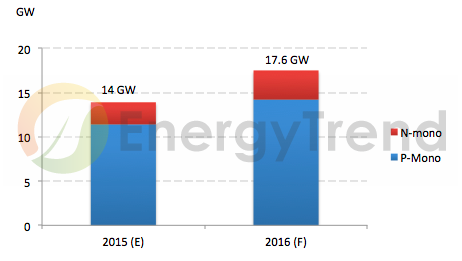

Cost is the fundamental factor to staying competitive in the PV market compared with other aspects such as technological advances, conversion efficiency and supporting policies. Therefore, whether mono-Si wafers can maintain their recently achieved US$0.10/pc price difference with the less costly multi-Si wafers will be crucial to market share growth of mono-Si products in 2016. As mentioned above, projected global mono-Si demand will be less than 10GW this year, but global mono-Si wafer capacity has already reached 14GW this year. This oversupply has led to a substantial price drop in the mono-Si wafer market. Looking ahead to 2016, wafer manufacturers will be expanding their mono-Si capacity as they are optimistic about the market prospects. Major Chinese wafer suppliers that have confirmed to making such plans are LONGi and Zhonghuan. Also, the leading multi-Si wafer company GCL has announced that it will increase its mono-Si wafer capacity to 1GW next year, marking an aggressive entry into this market. In sum, EnergyTrend projects that the global mono-Si capacity will surpass 17GW in 2016, with the annual growth rate exceeding 20%.

Figure 4: Global mono-Si wafer capacity, 2015~2016

Source: EnergyTrend

Nonetheless, oversupply will persist in the mono-Si wafer market next year unless end market demand increases substantially. For N-type mono-Si wafers, the supply and demand situation is more balanced because the customer base for these products is concentrated and stable. The market for P-type mono-Si wafers, by contrast, is already seeing a severe supply glut. Furthermore, top-tier wafer suppliers will be initially focusing on expanding their P-type mono-Si production next year. EnergyTrend therefore expects that it will be difficult for P-type mono-Si wafer prices to rebound above US$0.95/pc, so the price gap between mono- and multi-Si wafers will stay narrow.

The mono-Si segment is projected to account for 18% of the global PV demand in 2015. Besides building on this year’s results, the growth and development in next year’s mono-Si market will be driven by the following factors: the rise of the DG market, the low mono-Si wafer prices, the increase in conversion efficiency, the emergence of solutions to LID, and the maturation of PERC technology. Based on EnergyTrend’s analysis, the share of the mono-Si segment in the global PV demand for next year may grow to 25%, or 14.5GW out of the projected total demand of 58GW.