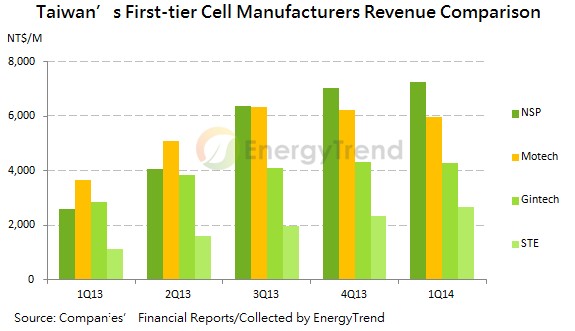

Impacted by increased demand from China, Japan, USA, and UK, PV installation is likely to grow substantially in 2014, and thus will lead to a surge in overall supply chain prices. “In 1H13, cell and module prices were the first ones to increase. Taiwan’s first-tier cell manufacturers – NSP, Motech, and Gintech, have started to turn losses around since 2Q13. Looking back to the financial results of 2013, major manufacturers’ gross margins in 3Q13 & 4Q13 reached a new high.” Said Corrine Lin, Analyst of EnergyTrend. Chinese module manufacturers can be profitable as long as they earn a gross margin of 15%. Among all Chinese manufacturers, Jinko Solar first turned profitable in 2Q13 due to their low-cost advantages. Trina Solar and Canadian Solar also became profitable in 3Q13 because of Trina’s record-breaking module shipment and Canadian Solar’s thriving power plant business. By 4Q13, JA Solar turned losses around at last. The year 2013 marked the turnaround of PV industry.

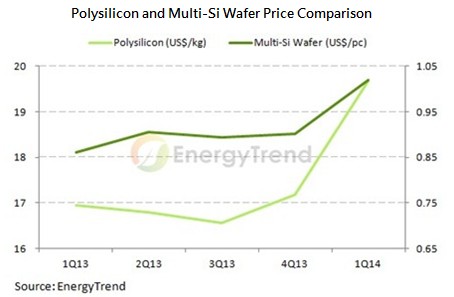

Manufacturers within PV supply chain are closely connected to one another. After downstream manufacturers got their benefits, upstream polysilicon and wafer manufacutrers then followed suit in the beginning of 2014. EnergyTrend’s price data showed, Polysilicon and wafer average prices maintained a positive growth every month in 1Q14. Polysilicon and multi-si wafer average prices increased more than 7% in January, respectively. Although spot prices have stopped increasing due to uncertainties caused by the US-China trade war, this year’s total demand continued to increase compared to last year’s. Therefore, manufacturers are positive about 2H14 demand, getting ready for capacity expansion.

Polysilicon Supply Shortage Issue May Appear Again

Polysilicon prices obviously increased this year, which motivated polysilicon manufacturers to expand their capacities. Due to high utilization rates, first-tier Chinese manufacturers - GCL, TBEA, and Daqo New Energy are planning to expand their capacities in Western China where there are rich resources and cheap electricity prices; Second-tier Chinese polysilicon manufacturers may follow their steps as well; Japanese and Korean manufacturers have started to get ready for expansion or use debottlenecking/re-activated production lines to raise polysilicon production. Since Taiwan’s polysilicon prices have reflected an uptrend this year, it’s projected that production output this year will increase significantly from last year. But overall, polysilicon spot prices are still lower than many manufacturers’ costs. If all manufacturers expand their capacities to lower costs and gain advantages, polysilicon supply issue may appear again.

Cell Emphasizes on Efficiency, Production Capacity did not Expand Significantly

For cell, capacity of Taiwan’s top-three cell manufacturers exceeded 1.5GW. The Increased shipment has caused sales revenue to continuously reach a new record. Judging from Taiwan’s cell output, mono-si cell has higher conversion efficiency and lower temperature coefficient. Since distributed PV systems have become more popular nowadays, mono-si cell might be the mainstream product in the future. When it comes to capacity expansion, Taiwan’s first-tier cell manufacturers always focus more on mono-si production expansion, thus this year’s mono-si shipment account for larger proportion. In fact, Taiwanese manufacturers have showed their intensions for capacity expansion last year, yet, actual moves will have to wait until the US-China anti-dumping and countervailing results are confirmed. At this point, there’s only one thing that can be sure – conversion efficiency. Because PV industry aims at higher efficiency, aside from the increased capacity in 2H14, conversion efficiency for mainstream cells will increase from 17.4% to 17.8%-18% due to the implementation of new production process and new paste. In the meantime, China’s first-tier vertically-integrated manufacturers are not planning for capacity expansions yet. They will still focus on merger and acquisition, which will have little impact on actual supply and demand.

Module Expansion Takes Place in China and Taiwan to Respond to Strong demand from China and Japan in 2H14

Both Chinese and Taiwanese module manufacturers have expansion plans. In regards to Taiwan, Japan has been a major export country for Taiwanese modules. Although less people have installed PV systems as Japan’s fiscal year came to an end, there are still 20GW of power plants waiting to be connected to the grid after Japan implemented new subsidy plans in July, 2012. In another words, an average capacity of more than 8GW-10GW still has to be installed every year in the next two years. That’s why demand remains strong even though less people install PV systems in 2Q14. Estimated from the customs data announced by the government, Taiwan’s module export volume was around 470MW in 2013, in which, 43% of the modules were shipped to Japan. Furthermore, Taiwan’s module export volume to Japan in 1Q14 was equivalent to half of the export volume to Japan last year, which reached a new high. Taiwan’s cell manufacturers have begun to plan for module expansion in order to meet Japanese clients’ OEM orders. It’s expected that things will be clearer as the US-China anti-dumping and countervailing result is finalized. There will be some changes to Taiwanese manufacturers within the module segment in 2H14.

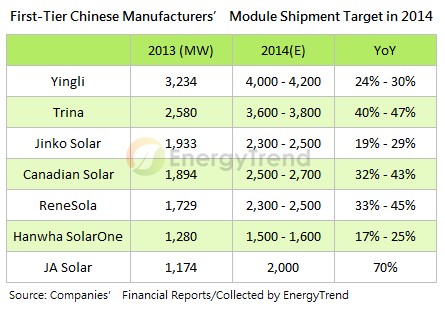

In terms of China, module export value to Japan has slowly increased since 2H13. China’s total module export value to Japan in 1Q14 exceeded US$1.3 billion, representing 40% (was 30% in 2013) of the total module export value. Overall, Chinese module shipment to Japan in 1Q14 reached a new high thanks to the increased PV installation before Japan’s fiscal year ended. It’s a milestone for first-tier Chinese vertically-integrated module manufacturers to stand firm in the Japanese market. On the other hand, this year’s strong Chinese demand has led to the increased shipment to China. Hence, first-tier manufacturers’ module shipment can be substantial, a 20%-40% rise compared to last year.

Manufacturers’ Gross Margins have Reached its Maximum, Supply and Demand Situation will be Critical in 2H14

Looking into 2014, the US-China anti-dumping result is postponed followed the delayed announcement of the anti-subsidy initial judgment. After Taiwanese cell manufacturers earned outstanding sales revenue in 1Q14, order condition in April and May was in good shape despite many uncertainties. As for Chinese manufacturers, costs will remain stable in the short run. First-tier manufacturers’ gross margins have increased further as 1Q14 financial results were being released. But they did not increase significantly like 2Q13-4Q13 unless there are breakthrough performances within power plant business. Although sales condition is in good shape, expenditures required for expansion may be a financial burden if financial condition is not improved.

Although demand from the US has turned weaker in 2Q14, demand from China, Japan and UK will continue to increase. In a word, there will be an entire different image to PV industry in 2H14 due to stable supply and demand status, disregarding the impacts cause by the US-China trade war.