A number of positive signs are starting to emerge regarding the U.S. economy, but there remain political and global headwinds that could slow growth, according to a new report.

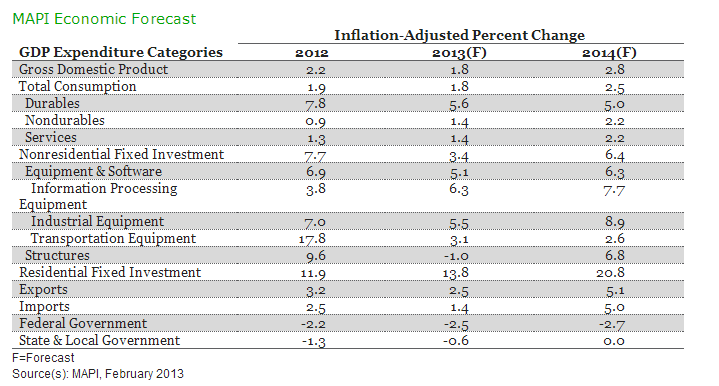

The Manufacturers Alliance for Productivity and Innovation (MAPI) Quarterly Economic Forecast predicts that inflation-adjusted gross domestic product (GDP) will expand by 1.8% in 2013 and by 2.8% in 2014, showing no change from MAPI’s November 2012 report. Manufacturing production, however, is expected to show growth of 2.2% in 2013 and 3.6% in 2014. The 2013 figure is an increase from 2.0% and the 2014 estimate is up from 3.2% from the November forecast.

There are mixed signals regarding employment prospects. Manufacturing is expected to see a net increase in hiring, with the sector expected to add 87,000 jobs in 2013, below the November forecast of 163,000 jobs. The outlook is for an increase of 289,000 jobs in 2014, a slight increase from the 270,000 previously forecast.

“There are several reasons to be optimistic about continued economic growth in 2013 and 2014,” noted MAPI chief economist Daniel J. Meckstroth, Ph.D. “Consumer deleveraging is close to an end; there are definitive signs of improvement in the housing market, especially on the supply side; and there is moderate job growth, pent-up demand, and the potential for spending that was previously postponed.”

Meckstroth warns, though, that consumers will still be restrained somewhat in 2013 by the 2% payroll tax increase, and government at all levels—federal, state, and local—is in an austerity mode. Business investment could be sluggish because of a confluence of factors: the recessions in Europe and Japan have hurt foreign affiliate earnings and limited U.S. exports; the deceleration of growth in China, Brazil, and other developing countries increases risks of a global slowdown; and there remains a level of uncertainty about federal policy and the resolution of policy deadlines.

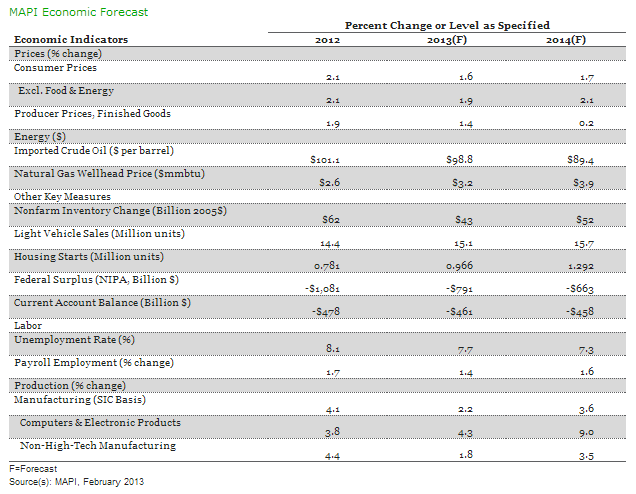

Production in non-high-tech industries is expected to increase by 1.8% in 2013 and by 3.5% in 2014. High-tech manufacturing production, which accounts for approximately 10% of all manufacturing, is anticipated to grow 4.3% in 2013 and 9.0% in 2014.

The forecast for inflation-adjusted investment in equipment and software is for growth of 5.1% in 2013 and 6.3% in 2014. Capital equipment spending in high-tech sectors will also rise. Inflation-adjusted expenditures for information processing equipment are anticipated to increase by 6.3% in 2013 and by 7.7% in 2014.

MAPI expects industrial equipment expenditures to advance by 5.5% in 2013 and by 8.9% in 2014. The outlook for spending on transportation equipment is for growth of 3.1% in 2013 and 2.6% in 2014. Spending on nonresidential structures will decrease by 1% in 2013 before improving by 6.8% in 2014.

Inflation-adjusted exports are anticipated to improve by 2.5% in 2013 and by 5.1% in 2014. Imports are expected to grow by only 1.4% in 2013 but rebound to 5% in 2014. MAPI forecasts overall unemployment to average 7.7% in 2013 and 7.3% in 2014. “Moderate economic growth will allow for some continued but relatively slow improvement in the unemployment rate,” Meckstroth said.

The refiners’ acquisition price per barrel of imported crude oil is expected to average $98.80 per barrel in 2013 and $89.40 in 2014.