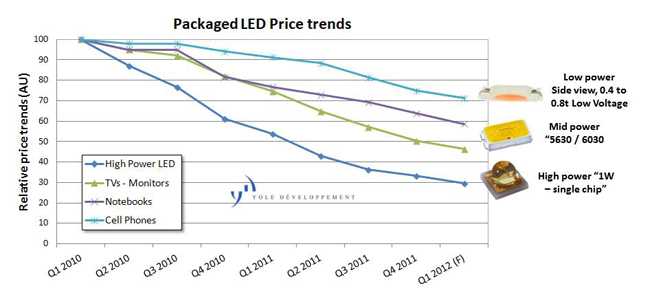

LED utilization rates are picking up again, with utilization in Taiwan now back up to 70 to 90 percent of capacity. Companies expect to be back to close to 100 percent in a month or two, driven by TV backlight demand, reports Yole Développement senior analyst Eric Virey. And Asian producers see demand for general lighting starting to pick up as well, expecting general lighting—mostly replacement bulbs— to account for 10 to 30 percent of company revenues by the end of the year. “It’s already becoming a commodity product— even before being popular,” says Virey. “It’s now so competitive with so many light bulb suppliers, though only a few are of good quality, that it’s pushing prices down quickly, so margins are shrinking fast.”

Source: Yole Développement

“In a commodity market— and we think this is a commodity market— the guy with the lowest cost structure wins,” no tes Jed Dorsheimer, managing director, equity research, lighting & solar, Canaccord Genuity. “And yield is by far the most important driver of costs.” With best industry net yields still at some 75-80 percent, and the majority around 50 percent, there’s plenty of room for improvement, particularly in automating the post epi processing, by using semiconductor industry style automation, steppers, and improving the liftoff, thinning, dicing and sorting processes. Last year’s 50 percent drop in prices really focused people’s attention on cost structure, and is speeding up the investment in automating these BEOL processes.

Summary of LED Package Price and Performance Projections

| Metric | 2011 | 2013 | 2015 | 2020 | Goal |

| Cool White Efficacy (lm/W) |

135 |

164 |

190 |

235 |

266 |

| Cool White Price ($/klm) |

9 |

4 |

2 |

0.7 |

0.5 |

| Warm White Efficacy (lm/W) |

98 |

129 |

162 |

224 |

266 |

| Warm White Price ($/klm) |

12.5 |

5.1 |

2.3 |

0.7 |

0.5 |

Caption: Though cost and especially efficiency of LED lighting has improved impressively recently, there are still major improvements necessary to meet the aggressive target price per lumen output needed for wide adoption according to the industry consensus roadmap put together by the US Department of Energy. It figures the cost for warm white packaged LEDs was about $12.50/klm as of last year, and targets a drop to $5.10/klm by next year, to stay on target for $2.00/klm by 2015. Notes: Projections for cool white packages assume CCT=4746-7040K and CRI=70-80, while projections for warm white packages assume CCT=2580-3710K and CRI=80-90. All efficacy projections assume that packages are measured at 25°C with a drive current density of 35 A/cm2; Package life is approximately 50,000.(Source: US DOE Solid State Lighting R&D Multiyear Program Plan, April 2012)

The choice of substrate material is naturally the first driver of yield, where it may turn out that high-cost, homogenous GaN substrates with very low defect density and potentially high yield could turn out to be a low cost choice, argues Dorsheimer. Silicon substrates seem like a low cost alternative, but even if fully depreciated equipment brings the typical 20 percent capital cost to zero, and low substrate costs bring the typical 15 percent substrate cost to zero, lower yields could still make GaN on Si more expensive than sapphire or SiC.

The Potential for GaN and Si Substrates

LED devices made on silicon now look likely to be able to match the performance of conventional devices on sapphire, reports Virey, as work at a number of labs around the world is closing the performance gap. So the crucial issue is really the cost savings from being able to use highly efficient 8-inch silicon processing equipment. Yole cost simulations show a 50 percent reduction in die cost is possible, and some companies project as much as 75 percent savings, at least compared to smaller diameter sapphire, depending of course on yield, on how much the producer has to invest in new facilities, and on how much retrofit is needed to convert a CMOS fab to LED production. With the biggest impact on yields in epi now apparently not from dislocation defects but from bowing during the MOCVD process, fine tuning the thermal properties during epi could potentially bring significant improvement.

But it does open the possibility of an almost fabless model for LED makers who could produce in CMOS foundries. And it could certainly change the industry supply equation. “One CMOS fab probably has enough capacity for the world’s supply of LED die,” notes Virey. GaN-on-GaN should have better yields from less bowing, and has advantages for being able to inject more current to get more light out of a smaller chip area, for high current density applications. But with the leading conventional LEDs on sapphire or SiC now up to 200lm/W efficiencies, closing in on the theoretical limit, the 5 to 10 percent increase in performance possible with the GaN substrate may not be worth the 10x higher substrate cost. Here again, it’s just a cost game where yield is the critical parameter.

Lattice Power Pushes towards Mass Production with GaN-on-Si

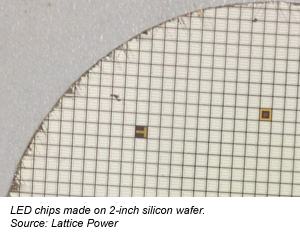

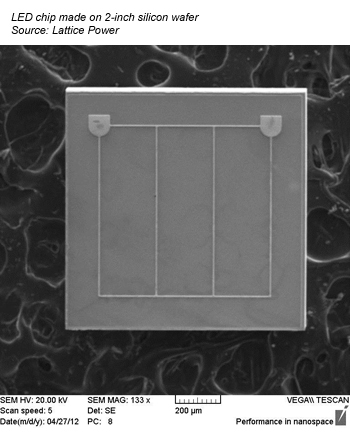

Lattice Power reports it is now selling commercial LED die from volume production runs of several hundred 2-inch silicon wafers a day from its Jiangxi, China, fab, and aims to transition to 6-inch wafers within twelve months. “We’re not in R&D mode anymore, we’re pushing towards mass production,” says CTO Hanmin Zhao. He reports performance, cost and yields in the 2-inch silicon are similar to 2-inch sapphire, and reliability and life test have so far shown results similar to sapphire.

Lattice Power reports it is now selling commercial LED die from volume production runs of several hundred 2-inch silicon wafers a day from its Jiangxi, China, fab, and aims to transition to 6-inch wafers within twelve months. “We’re not in R&D mode anymore, we’re pushing towards mass production,” says CTO Hanmin Zhao. He reports performance, cost and yields in the 2-inch silicon are similar to 2-inch sapphire, and reliability and life test have so far shown results similar to sapphire.

Zhao says the company’s solution for designing and then growing the multi-layer buffer layers to counter the lattice and thermal mismatch seems to transition fairly well to 6-inch wafers, where the advantage of silicon would of course be much more significant. It’s looking at 6-inch because the tools would be affordable, while it needs a partner with an idle 8-inch IC fab to make production on 8-inch silicon economical with the more expensive tool cost, and there are not many idle 8-inch fabs in China. Zhao figures that except of course for the MOCVD equipment, some 70-80 percent of the CMOS tools could be used with only minor modification.

Zhao says the company’s solution for designing and then growing the multi-layer buffer layers to counter the lattice and thermal mismatch seems to transition fairly well to 6-inch wafers, where the advantage of silicon would of course be much more significant. It’s looking at 6-inch because the tools would be affordable, while it needs a partner with an idle 8-inch IC fab to make production on 8-inch silicon economical with the more expensive tool cost, and there are not many idle 8-inch fabs in China. Zhao figures that except of course for the MOCVD equipment, some 70-80 percent of the CMOS tools could be used with only minor modification.

These speakers will join other industry leaders from Cree, Everlight Electronics, Soraa, Seoul Semiconductor, GT Advanced Technologies, EVGroup, Laytec and more to discuss the potential of disruptive technologies and best options for improving manufacturing yields in LED manufacturing at Extreme Electronics (South Hall) at SEMICON West 2012, July 11, in San Francisco.