After a very strong second quarter of 2010, the photovoltaics market is on track to deliver more than 15 GW of installations in 2010 - more than double the 2009 figure and up slightly on the consensus figure arrived at earlier this year.

But the latest prediction from market analysts at Solarbuzz comes with a warning that the opening quarter of 2011 will provide suppliers with a major challenge. That is largely because of an expected slump in demand from Germany, the key market for installations, where legislators are to cut financial support for solar projects at the start of the new year.

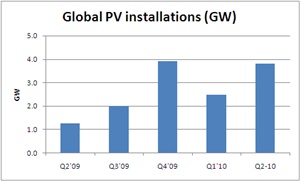

Craig Stevens, the president of Solarbuzz, said that demand in the second quarter of 2010 soared to 3.82 GW. That figure, although slightly lower than an earlier prediction of 4 GW from the same company, still represented a 54 percent increase on the opening quarter of 2010, and more than three times the level seen in the second quarter of 2009.

In fact, demand in the second quarter of 2010 was only marginally lower than the all-time record quarter – the 3.92 GW registered in the closing quarter of 2009.

"The rush to install in Germany ahead of tariff declines in mid-2010, combined with strong incentive programs across Europe, especially in Italy, France and the Czech Republic and an improved financing environment, drove the global PV market in Q2'09," Stevens reported.

Germany remains overwhelmingly dominant in the PV market, accounting for 60 percent of global demand in the latest quarter (2.3 GW). The next-largest installer is now Italy, where, despite a sequential doubling in demand, the market is just one-tenth that of Germany’s. Stevens also noted strong increases from the US and France during the period.

Supply side

In terms of supply, capacity utilization remains high, with wafer capacity remaining the most constrained part of the industry chain – even though 495 MW of wafer capacity was added during the second quarter of 2010.

Cell supply remains dominated by First Solar and an increasing influence of Chinese companies, with First, Suntech Power, JA Solar, Yingli Green Energy and Trina Solar making up the leading group of manufacturers. Out of the top 12 cell makers, six Chinese manufacturers now account for 55 per cent of shipments – compared with 43 percent just 12 months ago.

Cell production

With a steady balance between supply and demand now established, PV module prices have stabilized, and in Europe they even increased slightly during the quarter, noted Stevens. But the sharp price declines seen in the recent past means that modules are around 24 per cent cheaper now than they were at this time last year.

“Looking ahead into 2011, the most challenging quarter will undoubtedly be Q1,” says Stevens, forecasting the impact of the reduced feed-in tariffs. “Even with careful phasing of projects and price reductions, market demand is projected to be less than half of module production.”